THE MANDATE

The Amplify Transformational Data Sharing ETF (BLOK) is an actively managed fund, seeking to identify the leading companies focused on the transformation and development of the blockchain and cryptocurrency markets. The managers focus on how companies can capture the growth, innovation, and disruption of the blockchain paradigm shift. The evolution of the internet has changed how people communicate. We believe growth companies that embrace blockchain evolution will capture secular growth trends that are accelerating and disrupting core processes in business. We think this is an important secular trend, as Gartner forecasts business value generated by the blockchain could be $176 billion by 2025, and $3.1 trillion by 2030.

MARCH MONTHLY & FIRST QUARTER HIGHLIGHTS

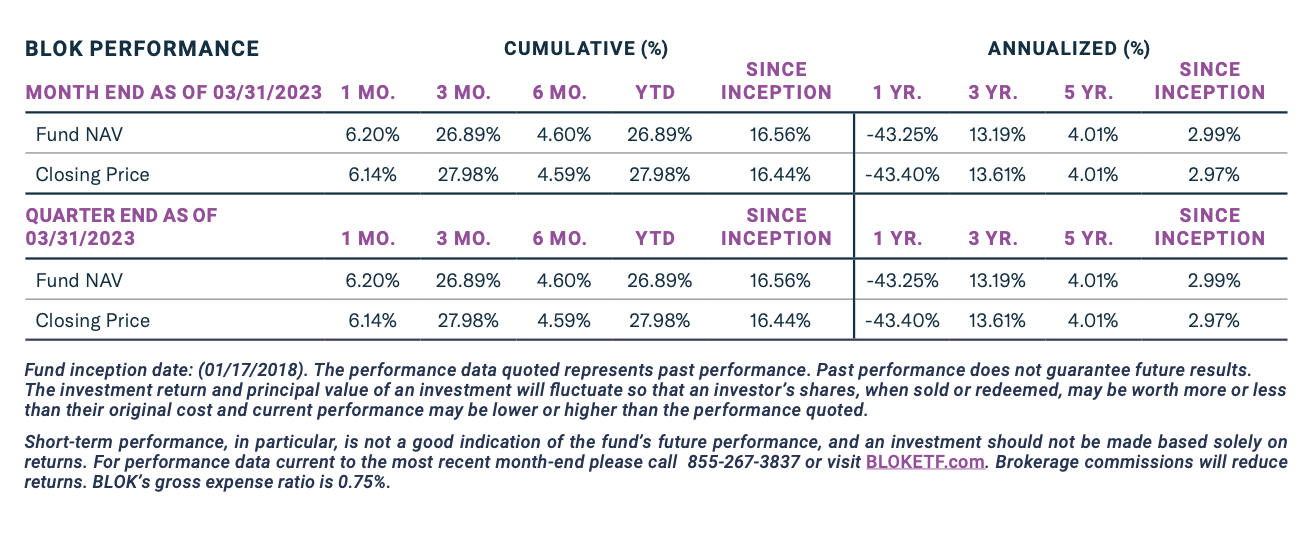

The fund rebounded 6.20% in March, and 26.89% overall in the first quarter of 2023. These rebounds were due to some strategic decisions we made late last year, as well as progressively throughout the quarter. Specifically, we reduced some of the defensive positions in Accenture and IBM and added to positions that were more correlated to the price action of bitcoin, like RIOT Platforms (RIOT), Marathon Digital (MARA), Bitfarms (BITF/BIT.CN), Hut8 (HUT/HUT.CN), HIVE Blockchain (HIVE/ HIVE.CN) and Galaxy Digital (BRPHF/GLXY.CN). We also added CleanSpark (CLSK) to the portfolio in March. These decisions strategically increased bitcoin mining exposure to about 20% and accelerated the fund’s momentum and correlation with bitcoin. At the beginning of the quarter this exposure was at a historic low of 9.5% - this was a meaningful pivot.

TWO REASONS FOR BITCOIN THE RALLY: BANKING CRISIS AND INCREASED UTILITY

We recognize that most investors are wondering where the price of bitcoin goes after such a significant bounce off the bottom. Our thinking is higher again. Why? First, passing through the Winter of 2022 and arguably extremely oversold conditions, the macro environment for a further bitcoin rally looks very consistent with past patterns and fundamentals. Bitcoin was born as a hedge against the “Great Financial Crisis of 2008,” and led to a bailout that has reached an estimated $498 billion, according to MIT Sloan. Given this foundational backdrop and its history of also rallying during the Cypriot financial crisis in 2013, during Brexit in 2016, and of course during the economic turbulence in 2020-2021, bitcoin’s rally in 2023 made sense to us. These are examples of why we think there are more legs in the rally. Unfortunately, we do not believe the banking crisis is behind us, so bitcoin makes sense as a hedge.

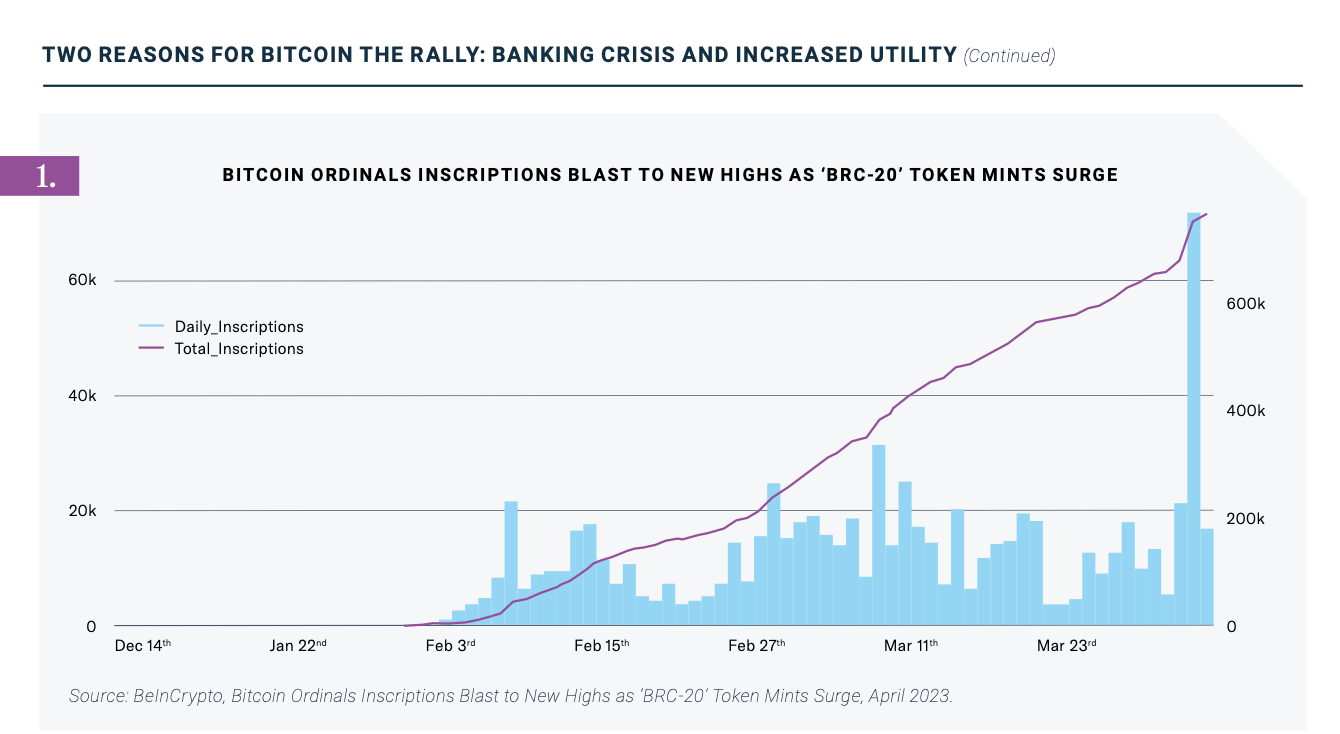

A second important rationale for continued momentum is the fact that the utility value of bitcoin has increased. Specifically, we are excited about the opportunity ahead for inscriptions and ordinals, which we highlighted in our February blog. Galaxy Digital Research explains the opportunity as being a $5 billion incremental boost for bitcoin utility value. It is difficult for people who don’t program to appreciate the opportunity here, but note that March follows February with a new record of excitement and utility value around bitcoin and this additional use case. Essentially, what this all means, is that along with the security that the bitcoin network provides through the miners, coders can now write script to build Non-Fungible Tokens (NFTs) on bitcoin “ordinals” rather than just using smart contracts on Ethereum. This is important to the miners because if the momentum continues to build, it could add significant additional revenue to the miners as NFTs drive processing revenues associated with transaction volume. As a reminder, NFTs are more than pictures. They can also host intellectual property that involves transactional types of metadata that ultimately leading to a permanent record (see Fig. 1). Could this be an evolution of the most secure coding platform ever designed?

Again, the most straightforward places the portfolio gets bitcoin correlation from are the portfolio categories in direct exposure and Bitcoin Miners. Direct exposure to bitcoin comes through the investments in 3 Bitcoin Spot ETFs, MicroStrategy, Equity, and Bonds at 10.11%. The exposure across 7 bitcoin miners was increased throughout the quarter to 20.31%, up from 9.5% at the conclusion of December 2022. While we are believers in portfolios that provide high active share and high conviction ideas, we do seek a level of diversification to provide risk controls across 40 to 60 holdings. Currently, the fund holds 48 positions.

PORTFOLIO TRANSACTIONS & OUTLOOK

BLOK, of course is more than just bitcoin. Our mandate is about the transformation of data sharing, and this is about the Blockchain. To this point, while we trimmed Walmart, Accenture, and IBM during the quarter, this was done for short term interest. We continue to believe that these firms are early adopters of the technology. In March, it should be noted that we added to the position in Customers Bancorp (CUBI) on the Monday after the FDIC took over Silicon Valley Bank and Signature Bank. Given our concerns about the banking crisis, the decision to add even a small amount of exposure to the bank sector was not made lightly and comes after we had sold our complete positions in Signature Bank (SIVB) and Silvergate (SI) earlier in the quarter. We expect to keep these exposures narrowly focused to include New York Community Bank (NYCB), which recently won a substantial mandate from the FDIC to complete an acquisition of part of Signature Bank. In the press release, NYCB highlights this acquisition is expected to be accretive. The rational for these two positions, which in aggregate make up 3.69%, is a clear reflection of our views about the risk/reward tradeoff, the long-term opportunities, and their differentiated focuses on Blockchain. In the case of customers, we believe that the firm could benefit from indirect deposit growth caused by the disruption at Silicon Valley Bank and Signature Bank/New York NY (SBNY). Bank balance sheets today are fluid, which makes due diligence a challenge on both the long and short side, but our research on the additional investment was further validated by the CEO’s purchase of additional stock. We believe that Customer’s exposure to crypto is limited to just taking deposits in USD. We would point out NYCB did not expressly take $4 billion in deposits related to firms involved in crypto. NYCB has a leadership position for processing HELOC’s on the blockchain in 5 minutes for delivery in 5 days.

The exposure to venture capital and early-stage companies is limited, but in strong times we have highlighted how venture capital will play a role in funding growth of the blockchain. While we see no reason to change this outlook and vision, it is important to note that venture capital investing in the area for the first quarter of 2023 is down about 53%, from $162 billion to $76 billion according to Yahoo finance and Crunchbase. Further to the point, these numbers include two particularly large deals - $10 billion in ChatGPT and $6.5 billion in Stripe. According to the same sources, this also means that some $580 billion remains available as dry powder. Furthermore, as the Crunchbase article by Gene Teare observes, “Many multistage investors pivoted away from late-stage but kept their seed practices open, informed by the 2008 crisis when some of the most critical companies — including Square, Airbnb, Uber, WhatsApp, and Slack — were started during that period. That downturn, after all, coincided with two major technology trends: the growth of cloud computing and the advent of smartphones.” An example of this in our portfolio could be Overstock’s 15-20% position in Grainchain, and other holdings in the Medici portfolio. We believe the impact that farmers feel from this Blockchain disruptor is quite exciting, as it could show a revenue run rate of $100 million run rate within the next 4 quarters. We anticipate more to follow in May, at the 2nd Annual Pelion Venture Medici Portfolio review webinar. The 11.38% allocation to venture capital remains relatively concentrated across 3 companies: Overstock (3.60%), SBI Holdings (3.78%), and Galaxy Digital (4%). We think these companies are particularly misunderstood by the markets because they do not fit in a neat package for analysts and investors, and as such, will add substantial upside surprises to the portfolio.

EDUCATION

For those who just want to get educated on the blockchain, here are some links:

■ The banking crisis, how to prepare: https://www.reventure.app/blog/more-bank-failures-are-coming-heres-how-to-prepare

■ Blockchain explained in a video: https://www.youtube.com/watch?v=ru_vu-T0hd8

■ Satoshi Nakamoto Original Bitcoin White paper: Bitcoin: A Peer-to-Peer Electronic Cash System https://bitcoin.org/bitcoin.pdf

SUMMARY

The Fund rebounded 26.89% in Q1, which included 6.20% in the month of March. This was partially a result of some strategic repositioning in the fund throughout the quarter. To this point, while bitcoin rallied, we actively increased exposures to highly correlated positions to such price action. Bitcoin miners now are at 20.31% of the portfolio, up from 9.5% at the close of 2022. After bottoming in 2022, the 2023 Bitcoin rally is consistent with its fundamental intent, as solution to inevitable financial crisis. This, on top of blockchain technology increasing the utility value of bitcoin, should build on the momentum.

These are challenging and exciting times! If you are an investor in BLOK, please know we appreciate your confidence and willingness to continue on this journey with us. We are open to questions and all inquiries, even if they challenge us!