The stock market has been supported by a healthier-than-expected economy this year, generating returns that have helped many portfolios to partially recover from last year’s bear market. Investors now hope these growth trends will translate into stronger corporate earnings since, in the long run, markets tend to follow the same trajectory as profits. With the future of the economy still uncertain, what signs are there that companies might begin to see improved profitability?

The third quarter earnings season is nearly wrapped up with almost all S&P 500 companies reporting their results. This is likely to be the first quarter of positive growth in a year, a notable inflection point that mirrors the surprising stability of the underlying economy. Consensus Wall Street estimates are for earnings to be flat this year at about $217 per share but to then rebound in 2024 by 11%. While this is somewhat at odds with economic forecasts for slowing growth in the coming quarters, it’s safe to say that any acceleration in earnings would be welcomed by investors.

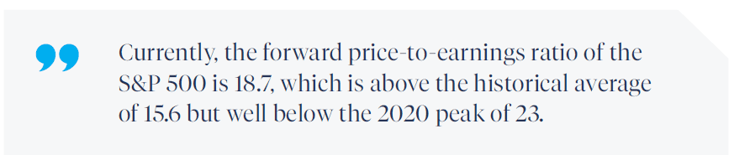

As the accompanying chart shows, the growth of corporate profits has been slowing since its peak in 2021 but may have reached a turning point. Historically, large public companies have increased their earnings by an average of 7.7% per year, but this fluctuates alongside the business cycle. To oversimplify the earnings cycle, in good times companies increase their sales faster than their expenses, boosting profits and margins. In bad times, companies experience slowing revenues and cut costs to maintain margins. Better cost structures then allow companies to be more profitable once the economy turns around.

As the accompanying chart shows, the growth of corporate profits has been slowing since its peak in 2021 but may have reached a turning point. Historically, large public companies have increased their earnings by an average of 7.7% per year, but this fluctuates alongside the business cycle. To oversimplify the earnings cycle, in good times companies increase their sales faster than their expenses, boosting profits and margins. In bad times, companies experience slowing revenues and cut costs to maintain margins. Better cost structures then allow companies to be more profitable once the economy turns around.