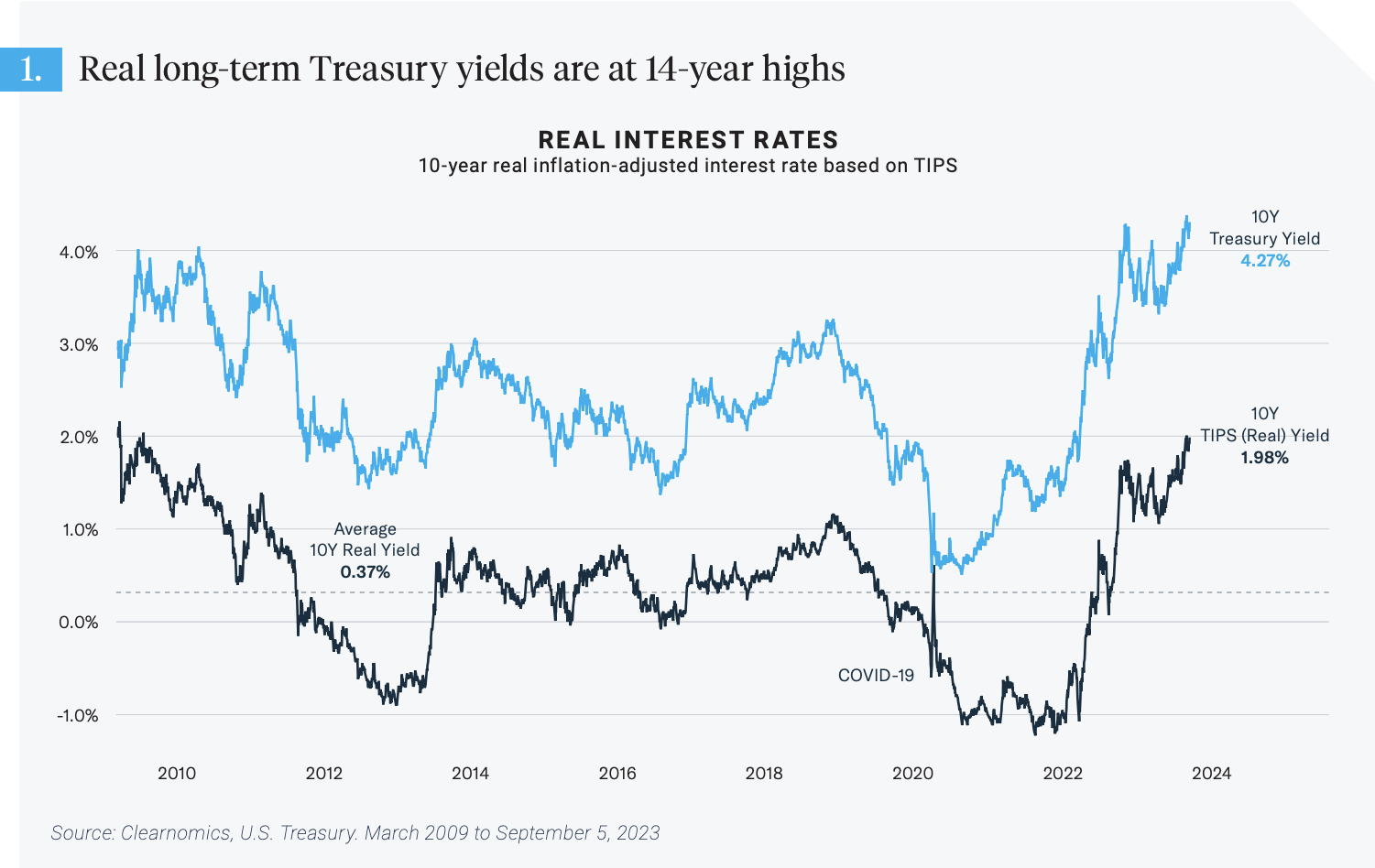

Long-term interest rates have come full circle over the past year. After falling as low as 3.3% during the banking crisis earlier this year, the 10-year U.S. Treasury is now yielding around 4.2%. However, while today’s long-term yields look similar to last year’s on paper, they are quite different from an economic and market perspective. What are interest rates telling us today and how does this impact long-term investors?

An important concept in economics is the distinction between “nominal” and “real” values. The simplest way to understand the difference is that nominal values include the effects of inflation while real ones do not. For instance, the price of a gallon of milk at the grocery store is a nominal price since it changes based on inflation. The paychecks we receive are also nominal values since they are paid in dollars or other currencies whose purchasing power changes as the prices of goods and services fluctuate.

A real value, on the other hand, represents the actual amount of goods and services one receives, irrespective of the prices of those items. A gallon of milk, for instance, is still a gallon of milk whether it costs $3.97, as it does today on average across the country, or $2.84 as it did five years ago. If someone were to receive their paycheck not in a set amount of nominal dollars but in the real dollar equivalent of gallons of milk, i.e. an amount that allows them to buy a set number of gallons, they would receive more dollars today. In this way, their paycheck would be protected from inflation, at least in terms of milk.